As interest rates have reached record-high levels, the property market in Belgium has cooled down. The Brussels Times asked Bart van Opstal of the Federation of Notaries what this means for people looking to buy property at the moment.

While the start of the pandemic initially triggered a slowdown in the property market, the aftermath was characterised by a rush for real estate as buyers bid for bigger spaces and properties with gardens. This wave of purchases saw property prices in Belgium skyrocket: between 2018 and 2023 the average house price rose from €253,608 to an average of €320,937.

However, this rush for real estate seems to have calmed in the country, and in the first half of this year, the number of real estate transactions across Belgium even decreased compared to last year.

Effect of interest rate

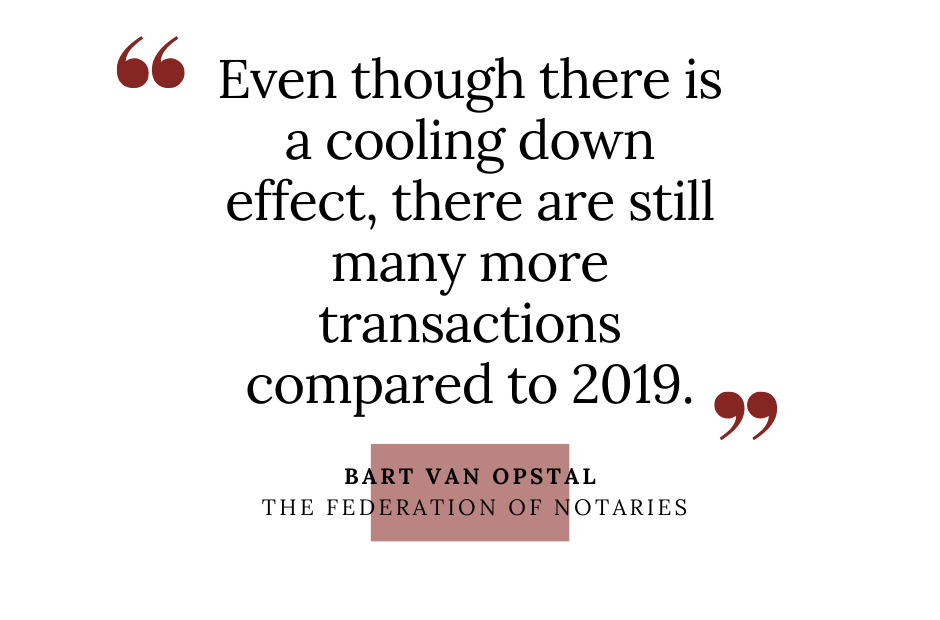

Van Opstal explained that this decline in transactions is mainly the result of the fact that the housing market in Belgium was at an exceptionally high level after the post-pandemic boom. "Even though there is a cooling down effect, there are still many more transactions compared to 2019." This also means that prices overall are still much higher than four years ago.

The decline in the activity is also partly a result of the rising interest rates. Last month the European Central Bank (ECB) raised interest rates by 25 basis points (0.25 percentage points) to a record high of 3.75% to curb continuously high inflation levels. A further slight rise in interest rates is expected later this year.

Van Opstal did add that the rise in inflation also resulted in people's wages going up due to Belgium's automatic wage indexation system. "That, in part, compensated for the rising living costs, but that also means that your borrowing capacity increases," which he argued partly counteracted the interest rate rise.

Van Opstal did add that the rise in inflation also resulted in people's wages going up due to Belgium's automatic wage indexation system. "That, in part, compensated for the rising living costs, but that also means that your borrowing capacity increases," which he argued partly counteracted the interest rate rise.

In the second half of last year, it helped more people under 30 enter the property market, not because prices were cheaper, but because they assumed interest rates would continue to rise in 2023. "In retrospect, they did the right thing because they were able to get a loan with a fixed interest rate, which has now risen, but their wages have also gone up because of the indexation of wages, so they did make the right decision at the time."

Further drop possible?

A recent study by Dutch bank ING noted that the high interest rates will continue to have an effect on house prices, saying that they are expected to fall by 3% in the second half of the year. It pointed to a sharp rise in selling times, indicating that a reversal in prices is imminent.

The banking group argued that while Belgium's wage indexation and an increase in loan terms have supported the property market so far, they are "insufficient to offset the rise in interest rates," which on average is about 3.5% for Belgians now borrowing with a 20-year maturity, amounting to an 11% drop in borrowing capacity.

A recently sold flat in Brussels. Credit: Belga

Van Opstal agreed that the hike in interest rates has had a restraining effect on the market and that this could see the market cool down further, especially if interest rates are further increased. The question now is whether the market will continue to cool down enough to make buying property more affordable, as credits have risen and property prices remain much higher than before the pandemic.

"If you look at the past period, we recorded price drops in Wallonia and in particular in Brussels, where the prices decreased by 4%. This is not nothing, but of course, we're still at an average price of €536,00 now, so it's not that Brussels has suddenly become ridiculously cheap," van Opstal said. For example, the price of a house in the capital has risen by almost a quarter (23.7%) in the last five years.

Impossible predictions

Van Opstal stressed that it is almost impossible to predict what will happen in the coming months.

"We don't know what inflation will do, and as a result what interest rates will do, but more importantly, what the effect will be on people," he said. If interest rates stabilise earlier in the second half, then that inhibiting effect of higher loans would lose some of its force, resulting in more transactions.

On the other hand, the market also depends a lot on inflation: if inflation goes down before interest rates, which is already happening, automatic indexation will freeze, meaning wage increases will not go up as fast. "This will also have an effect on the real estate market as the borrowing capacity of buyers will drop."

Related News

- 'Ixelles came late in the game': How property prices compared with Ganshoren over 40 years

- Belgian property taxes explode in last two years

- Brussels homeowners to be hit with record high property taxes

One thing is for sure: the real estate market is defined by confidence, and in the past, there has always been a huge amount of confidence in the Belgian market due to the so-called "brick" in the stomachs of the country's residents, which is much stronger than in other countries.

This was reflected in the fact that the Belgian property market held strong during the past crises, while in Germany, the Netherlands and France, prices already dropped well below their peak levels.

"Chances are there might be slight price drops in the coming months, but I don't think people should expect massive ups and downs. I think we have to accept to some extent that the period of very cheap credit and lower property prices is behind us, and probably won't come back soon," he concluded.